Published on Sep 3, 2025

Daily PIB Summaries

PIB Summaries 03 September 2025

Content

- The Income Tax Act, 2025

- Pradhan Mantri Formalisation of Micro Food Processing Enterprises (PMFME)

The Income Tax Act, 2025

Background and Evolution

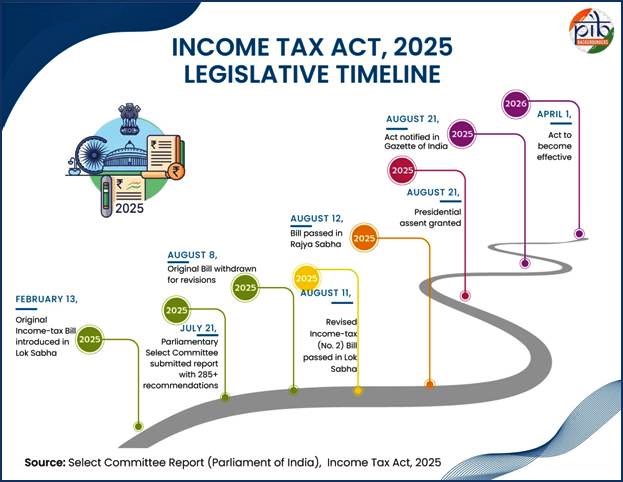

- Earlier framework: Income-tax Act, 1961 governed direct taxes in India for 64 years.

- Complexity problem:

- Amended ~65 times, with 4000+ changes.

- Multiple exemptions and deductions → reduced tax base.

- Outdated legal language → inaccessible to common taxpayers.

- Fragmented structure + litigation-heavy provisions.

- Reform process:

- Announced in July 2024 by Finance Minister.

- Drafted after stakeholder consultations and Select Committee review.

- Parliament passed Income-tax (No. 2) Bill, 2025 → effective 1st April 2026.

Relevance : GS 3(Economy – Taxation), GS 2(Governance)

Rationale for the Reform

- Simplify overly complex tax law.

- Reduce litigation and compliance burden.

- Remove obsolete provisions.

- Make law digital-ready and aligned with global best practices (UK, Australia).

- Improve ease of doing business and voluntary compliance.

Guiding Principles

- Textual & Structural Simplification: Replace archaic legal jargon with plain English.

- No Major Policy Changes: Tax slabs and rates largely unchanged for continuity.

- Predictability: Focus on clarity, not revenue overhaul.

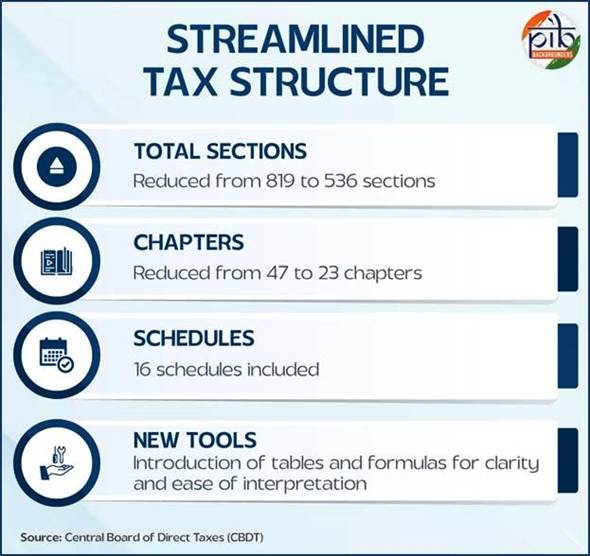

Key Features of Income Tax Act, 2025

A. Simplified Framework

- Fewer sections, reorganized chapters, structured schedules, and formulae.

- Example: TDS provisions consolidated into Section 393 (earlier scattered).

B. Tax Year Concept

- Replaces confusing “Assessment Year” & “Previous Year” with “Tax Year”.

- Defined as April 1 – March 31 (financial year).

- Enhances clarity for taxpayers.

C. Power to Frame Schemes (Section 532)

- Government can design schemes to:

- Minimize human interface via technology.

- Improve efficiency with functional specialization & economies of scale.

D. Digital-First Enforcement

- Virtual Digital Space defined (emails, servers, cloud, social media, trading accounts, websites).

- Virtual Digital Assets (VDAs): Broader scope including cryptocurrencies, tokenized assets, and other blockchain-based assets.

E. Simplified Compliance

- Streamlined filing, reduced redundancies.

- Emphasis on faceless assessments and digital compliance.

F. Dispute Resolution

- Robust taxpayer-friendly framework.

- Goal: reduce litigation backlog, improve trust-based tax culture.

Core Objectives

- Simplification: Modern drafting, clarity, reduced ambiguity.

- Digital Integration: Faceless assessment, online compliance, reduced corruption.

- Taxpayer-Centric Approach: Simplified filing, reduced litigation, transparency.

- Global Alignment: Recognition of VDAs, taxation aligned with global norms.

- Ease of Doing Business: Predictable, accessible, transparent tax framework.

Strategic Importance

- Reflects Atmanirbhar Bharat and Viksit Bharat @2047 vision.

- Enhances taxpayer trust → fosters voluntary compliance.

- Encourages digital economy adoption.

- Positions India’s tax system in line with global digital asset regulation trends.

Implications

- For taxpayers:

- Easier to understand rules, reduced confusion.

- Lower litigation burden.

- For businesses:

- Predictability, simplified TDS, clarity in compliance.

- Boosts investment climate.

- For government:

- Streamlined administration.

- Greater efficiency with technology-driven assessments.

- Potential to expand tax base by reducing exemptions.

Conclusion

- The Income Tax Act, 2025 is not a rate-change reform, but a structural clarity reform.

- It transforms taxation into a predictable, efficient, digital, and taxpayer-friendly system.

- A landmark shift from complexity → clarity, aligning India’s tax law with global best practices.

Pradhan Mantri Formalisation of Micro Food Processing Enterprises (PMFME)

Basics

- Launch: 29 June 2020, under Atmanirbhar Bharat Abhiyaan.

- Type: Centrally Sponsored Scheme (CSS).

- Duration: FY 2020-21 to FY 2025-26.

- Total Outlay: ₹10,000 crore.

- Cost Sharing:

- 60:40 → Centre: States.

- 90:10 → North-Eastern & Himalayan States.

- 60:40 → UTs with legislatures.

- 100% Centre → Other UTs.

- Coverage Goal: Support 2 lakh micro food processing units.

- Vision: “Vocal for Local in Food Processing Sector” → competitiveness, formalisation, job creation.

Relevance : GS 3(Economy & Food Processing) , GS 2 (Governance & SHGs)

Context and Need

- India has 25 lakh → 64 lakh registered food business operators (2020–2025).

- Food processing sector = vital link between agriculture and industry.

- Sector contributes significantly to:

- GDP (value addition).

- Employment (large rural base).

- Exports (USD 49.4 bn agri & processed food in FY 2024-25, ~20.4% from processed foods).

- Issues faced:

- High informality in micro food units.

- Lack of access to finance, branding, infrastructure, and technology.

- High post-harvest losses & wastage.

- PMFME fills the gap by formalising micro units and creating stronger value chains.

Key Achievements (as of June 2025)

- Funds released: ₹3,791.1 crore to States/UTs.

- Loans sanctioned: 1,44,517 loans worth ₹11,501.79 crore (Credit Linked Subsidy).

- Training: 1,16,666 beneficiaries trained.

- Seed capital support: Approved for 1,03,201 SHG members, ₹376.98 crore.

- FY 2024-25: 50,875 loans sanctioned under CLS.

- Component-wise approvals (till June 2025):

- Credit Linked Subsidy → 1,44,517 units (₹11,501.79 cr).

- Seed Capital → 3,48,907 members (₹1,182.48 cr).

- Common Infrastructure → 93 projects (₹187.20 cr).

- Branding & Marketing → 27 projects (₹82.82 cr).

Key Components

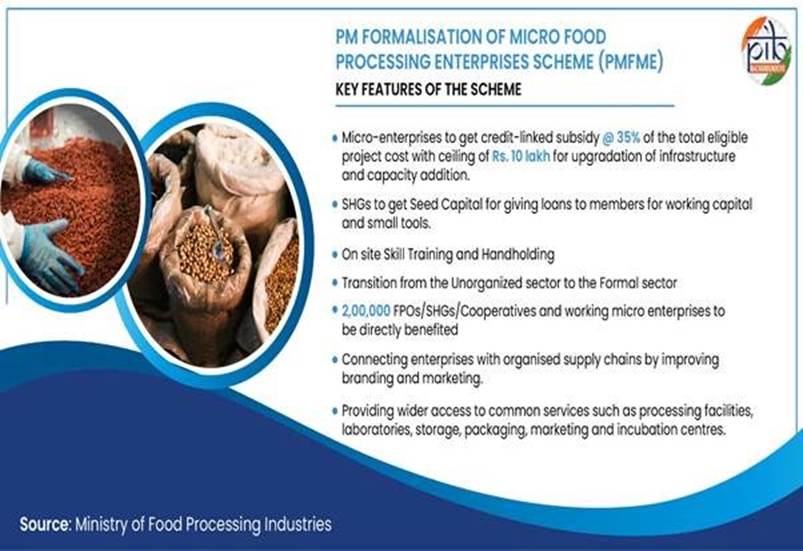

A. Support for Individual Units

- Credit-linked capital subsidy: 35% of project cost.

- Ceiling: ₹10 lakh per unit.

- Beneficiary contribution: Minimum 10%, balance via bank loan.

B. Support for Groups

- FPOs/Producer Cooperatives: 35% grant, training, credit linkage.

- Self-Help Groups (SHGs):

- Seed Capital: ₹40,000 per member (working capital, small tools).

- Priority to ODOP-linked SHGs.

- Disbursed as repayable loan via federation.

C. Branding & Marketing Support

- Target groups: FPOs, SHGs, Cooperatives, SPVs.

- Focus: ODOP products.

- Eligible activities:

- Common branding, packaging, standardisation.

- Tie-ups with retail chains & institutions.

- Quality certification & control.

- DPR support: up to ₹5 lakh for marketing/branding proposals.

D. Common Infrastructure

- Funded facilities:

- Assaying, sorting, grading, warehousing, cold storage.

- Common processing units for ODOP produce.

- Incubation centres for training + shared facilities.

Capacity Building & Research

- Lead institutes:

- NIFTEM (Kundli).

- IIFPT (Thanjavur).

- Collaborations: ICAR, CSIR labs, CFTRI, DFRL.

- Role: Skill development, R&D, product-specific training, technology transfer.

- Outcomes: 225 R&D projects, 20 patents, 52 technologies commercialised.

ODOP (One District One Product) Focus

- States/UTs identify priority products (fruits, vegetables, spices, fisheries, honey, turmeric, etc.).

- Objective:

- Promote local produce & traditional foods.

- Reduce wastage & post-harvest losses.

- Strengthen value chains (linking production, processing, marketing).

- Complement Agriculture Export Policy and cluster-based approaches.

Case Study

- Ruby Fresh Snacks, Ernakulam (Kerala):

- Started in 2011 with groundnut laddoos.

- PMFME loan (₹3 lakh in 2021) → purchased machines, expanded products.

- Profits increased from ₹12,000/day → ₹20,000/day.

- Turnover crossed ₹32 lakh in FY 2021-22.

- Showcases transformational potential of PMFME support.

Strategic Significance

- Rural development: Jobs, women empowerment (via SHGs).

- Formalisation: Micro units enter GST/FSSAI ecosystem.

- Value addition: Boosts farmer income and reduces food wastage.

- Exports: Enhances India’s processed food share in global markets.

- Economic resilience: Strengthens supply chains, aligns with Atmanirbhar Bharat.

Challenges & Way Forward

- Awareness gap among rural entrepreneurs.

- Delays in DPR preparation & credit disbursal.

- Quality standards and certification adoption need scaling.

- Need stronger retail & e-commerce linkages for ODOP brands.

- Sustainability of incubation centres and SHG-based enterprises.

Conclusion

- PMFME is a bridge between informal micro units and organised sector.

- Through credit, training, ODOP branding, and infrastructure, it transforms local producers into competitive entrepreneurs.

- Strengthens farm-to-market linkages, reduces wastage, boosts exports, and drives inclusive rural growth.

- A core driver of India’s ambition to become a global leader in food processing by leveraging local strengths.