Published on Jan 31, 2026

Daily PIB Summaries

PIB Summaries 31 January 2026

Content

- Economic Survey 2025–26

- Connectivity Projects under the Northeast Economic Corridor (NEEC)

Economic Survey 2025–26

Context

- Economic Survey 2025–26, tabled ahead of Union Budget, projects robust medium-term growth, historically low inflation, strong fiscal credibility, and resilient financial buffers despite adverse global economic conditions.

Background and context

- The Economic Survey is an annual, non-statutory policy document prepared by the Chief Economic Adviser, offering macroeconomic assessment, risk analysis, and reform priorities guiding fiscal and monetary policymaking.

Relevance

- GS 3 (Economy): GDP growth projections, inflation management, fiscal consolidation, capital expenditure, banking sector health, trade performance, external sector resilience, and financial inclusion.

State of the Indian economy: macro overview

Growth outlook

- India’s real GDP growth for FY27 is projected at 6.8–7.2%, with potential growth estimated around 7%, reflecting sustained demand, investment momentum, and structural reforms amid global uncertainty.

- First Advance Estimates indicate FY26 GDP growth at 7.4% and GVA growth at 7.3%, supported by agriculture recovery, manufacturing acceleration, and services-led expansion.

Inflation trends

- India recorded historic low CPI inflation averaging 1.7% during April–December 2025, driven by food and fuel disinflation, making it one of the sharpest inflation declines among EMDEs.

- RBI revised FY26 inflation forecast downward from 2.6% to 2.0%, while IMF projects 2.8% in FY26 and 4.0% in FY27, indicating a benign inflation outlook.

Sectoral drivers of growth

Agriculture and allied activities

- Agriculture is estimated to grow 3.1% in FY26, stabilising rural demand, supported by favourable monsoon, improved crop yields, and agricultural GVA growth of 3.6% in H1 FY26.

- Allied sectors like livestock and fisheries recorded stable 5–6% growth, enhancing income diversification, resilience, and reducing agriculture’s vulnerability to climatic shocks.

Industry and manufacturing

- The industrial sector is projected to grow 6.2% in FY26, with H1 growth of 7.0%, exceeding pre-COVID trends, signalling broad-based industrial recovery.

- Manufacturing GVA surged 7.72% in Q1 and 9.13% in Q2 FY26, reflecting structural revival driven by PLI schemes, infrastructure push, and improved corporate balance sheets.

- PLI schemes across 14 sectors attracted over ₹2 lakh crore investment, generated ₹18.7 lakh crore incremental output, and created 12.6 lakh jobs by September 2025.

Services sector

- Services grew 9.1% in FY26, with GDP share rising to 53.6% and GVA share to a historic 56.4%, underlining India’s transition towards a services-driven economy.

- India became the 7th largest services exporter, doubling its global share from 2% (2005) to 4.3% (2024), led by IT, financial, and professional services.

Employment and labour market trends

- Total employment reached 56.2 crore persons in Q2 FY26, with net addition of 8.7 lakh jobs, reflecting labour market resilience amid economic expansion.

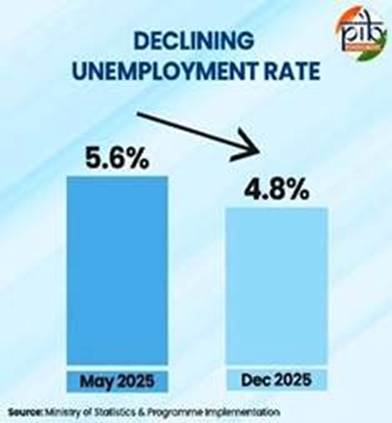

- PLFS data shows LFPR at 56.1%, female LFPR at 35.3%, WPR at 53.4%, and unemployment declining to 4.8%, indicating improved labour absorption.

- Organised manufacturing employment rose 6% YoY in FY24, adding over 10 lakh jobs, confirming industrial recovery translating into formal employment generation.

Trade and external sector performance

- India’s total exports reached USD 825.3 billion in FY25 and USD 418.5 billion in H1 FY26, driven primarily by services and non-petroleum exports.

- Services exports hit a record USD 387.5 billion in FY25, growing 13.6% YoY, reinforcing India’s global competitiveness in knowledge-intensive sectors.

- India’s share in global merchandise exports rose from 1% (2005) to 1.8% (2024), reflecting gradual integration into global trade networks.

External buffers

- Foreign exchange reserves stood at USD 701.4 billion (January 2026), providing 11 months import cover and covering 94% of external debt, strengthening external shock absorption capacity.

- India remained the world’s largest remittance recipient with USD 135.4 billion inflows in FY25, increasingly sourced from advanced economies, reflecting skilled workforce migration.

Industrial output indicators

- Index of Industrial Production (IIP) grew 7.8% in December 2025, highest in over two years, driven by manufacturing growth of 8.1%, mining 6.8%, and electricity 6.3%.

- Eight Core Industries Index showed strong momentum, with cement growth at 13.5% and steel at 6.9%, reflecting sustained infrastructure and construction demand.

Fiscal developments

Strengthened fiscal credibility

- India received three sovereign credit rating upgrades in 2025, reflecting improved fiscal discipline, revenue buoyancy, and commitment to capital-led growth.

Revenue and taxation

- Centre’s revenue receipts increased from 8.5% of GDP (FY16–20) to 9.2% of GDP in FY25, supported by buoyant non-corporate tax collections.

- Direct taxes’ share rose to 58.8% of total taxes in FY25, with income-tax filers increasing from 6.9 crore (FY22) to 9.2 crore (FY25).

Capital expenditure and debt

- Effective capital expenditure rose to 4% of GDP in FY25, sustaining growth while reducing general government debt-GDP ratio by 7.1 percentage points since 2020.

- Under Special Assistance to States for Capital Investment (SASCI), States maintained capital spending at 2.4% of GDP, supporting cooperative fiscal federalism.

Monetary and financial sector developments

Monetary policy and liquidity

- RBI reduced repo rate by 100 basis points to 5.25% during April–December 2025, complemented by CRR cut to 3%, enhancing credit availability.

- System liquidity remained in surplus at ₹1.89 lakh crore in FY26, aided by OMOs and forex swaps, supporting monetary transmission.

Banking sector health

- Gross NPAs declined to multi-decadal lows, with CRAR at 17.2%, ROE at 12.5%, and ROA at 1.3%, indicating strong banking sector fundamentals.

- Bank credit growth accelerated to 14.5% YoY in December 2025, with MSME credit expanding 21.8%, especially micro and small enterprises.

Financial inclusion and capital markets

- RBI Financial Inclusion Index improved from 64.2 (March 2024) to 67.0 (March 2025), reflecting enhanced access, usage, and quality of financial services.

- Household financialisation deepened, with equity and mutual funds share rising to 15.2% of savings in FY25, and household equity wealth increasing ₹53 lakh crore since 2020.

Conclusion: mains-ready synthesis

- Economic Survey 2025–26 portrays India as a resilient, high-growth economy with strong macro fundamentals, low inflation, robust fiscal credibility, deepening financial markets, and capacity to withstand global shocks while sustaining inclusive growth.

Connectivity Projects under the Northeast Economic Corridor (NEEC)

Why is it in news?

- In January 2026, the Government informed Parliament about progress under the Northeast Economic Corridor, PM-DevINE projects, and major road, rail, and digital connectivity expansion across the North-Eastern Region.

Relevance

- GS 2 (Polity / Governance): Cooperative federalism through NEC and HLTFs, Centre–State coordination, role of DoNER, digital governance via monitoring portals, and implementation capacity.

- GS 3 (Infrastructure / Regional Development / Security): Roads, railways, digital connectivity, PM-DevINE, logistics efficiency, employment generation, Act East Policy linkage, and strategic border connectivity.

Background and context

Strategic importance of the North-Eastern Region (NER)

- The North-East is strategically vital due to its international borders, Act East Policy relevance, security sensitivities, and historical infrastructure deficit, making connectivity central to integration and development.

Institutional trigger

- During the 72nd Plenary of the North Eastern Council (NEC) in December 2024, consensus led to creation of sector-specific High-Level Task Forces to accelerate economic transformation.

Northeast Economic Corridor (NEEC)

High-Level Task Force on NEEC

- A dedicated High-Level Task Force on NEEC, convened by the Chief Minister of Mizoram, was constituted to assess infrastructure gaps, investment ecosystem, and formulate corridor-based development strategies.

- The Task Force includes the Union DoNER Minister and Chief Ministers of Assam, Meghalaya, and Manipur, ensuring cooperative federalism and regional coordination in corridor planning.

Mandate and objectives

- The NEEC Task Force focuses on evaluating existing economic infrastructure, identifying logistics and connectivity gaps, and recommending policy measures to attract private investment into the North-East.

PM-DevINE scheme: development backbone

Objectives of PM-DevINE

- PM-DevINE aims at rapid and holistic development of NER through infrastructure creation, social sector projects, livelihood enhancement for youth and women, and bridging long-standing regional development gaps.

Project scale and funding

- Since inception, 48 projects worth ₹6,044.36 crore have been sanctioned under PM-DevINE up to January 2026, reflecting focused public investment in the North-East.

Road connectivity expansion

National Highways growth

- National Highway length in NER expanded from 10,905 km in 2014 to 16,207 km by April 2025, significantly improving inter-state and national connectivity.

- Currently, 177 highway projects covering 3,635 km, costing ₹87,119 crore, are under various stages of implementation across the region.

Rural roads under PMGSY

- Under PMGSY, 17,666 road works spanning 89,503 km and 2,396 bridges were sanctioned, strengthening last-mile connectivity in remote and hilly areas.

- Of these, 16,547 road works (81,448 km) and 2,126 bridges have been completed, with total expenditure of ₹53,353.49 crore, including State contributions.

Connectivity projects under MDoNER

- MDoNER sanctioned 647 road and bridge projects worth ₹8,260.88 crore, of which 500 projects costing ₹4,915 crore have already been completed, accelerating regional mobility.

- These projects focus on inter-district connectivity, border area access, and linking production clusters with markets, particularly in difficult terrain.

Rail connectivity in the North-East

Status of railway projects

- As of April 2025, 12 railway projects (8 new lines and 4 doubling projects) spanning 777 km and costing ₹69,342 crore were sanctioned in the North-East.

- Out of the sanctioned length, 278 km has been commissioned, improving passenger mobility, freight movement, and integration with national rail networks.

Structural constraint

- Railway projects are executed on a zonal basis, not State-wise, reflecting cross-boundary nature but also complicating coordination and monitoring in the North-East.

Digital connectivity expansion

BharatNet progress

- Under BharatNet, 6,355 Gram Panchayats in the North-East were made service-ready for high-bandwidth broadband connectivity by December 2025.

Mobile connectivity

- Under the 4G Saturation Project and allied schemes, 3,718 mobile towers have been commissioned, covering 5,366 villages and locations, reducing digital isolation.

Monitoring and governance mechanisms

Multi-layered monitoring framework

- Primary monitoring responsibility lies with State governments and implementing agencies, while DoNER oversees projects through Field Technical Support Units, Project Quality Monitors, and third-party inspections.

- Inspection reports are uploaded on the Poorvottar Vikas Setu portal, enabling transparent, real-time digital monitoring and accountability.

Integration with PM Gati Shakti

- Field units update project progress on the PM Gati Shakti National Master Plan portal, ensuring inter-ministerial coordination and reducing infrastructure silos.

Implementation challenges

- Project timelines are affected by difficult terrain, land acquisition constraints, statutory clearances, forest approvals, and logistical bottlenecks, common in the ecologically sensitive North-East.

Economic and strategic benefits

Economic integration and growth

- Improved connectivity enables faster movement of agricultural produce, essential goods, and industrial inputs, lowering logistics costs and enhancing market access for North-Eastern States.

Employment and livelihoods

- Infrastructure expansion generates direct construction employment and indirect opportunities in tourism, logistics, agro-processing, and small industries, supporting inclusive regional growth.

Strategic and social integration

- Enhanced connectivity strengthens national integration, improves border area accessibility, boosts security logistics, and aligns the North-East more closely with India’s economic mainstream.

Way forward: policy focus

- Corridor-based planning under NEEC should be aligned with Act East Policy, cross-border trade potential, and value-chain development to convert connectivity into sustained economic transformation.

- Greater private sector participation, faster clearances, and environmentally sensitive infrastructure design are essential to maximise returns on connectivity investments.

Mains-ready takeaway

- The Northeast Economic Corridor, supported by PM-DevINE and multi-sectoral connectivity expansion, marks a shift from infrastructure deficit correction to growth-oriented regional integration, strengthening economic, strategic, and social cohesion in the North-East.